I'm retired and own a freehold condo - should I downgrade to a HDB flat?

PHOTO: Stackedhomes

Because your Executive Apartment (EA) was originally a subsidised HDB flat, you will be considered a second-timer if you sell it and then buy another subsidised flat (e.g., a BTO flat). In this situation, HDB will require you to pay a resale levy.

This levy is imposed to reduce the housing subsidy on a second subsidised flat, making for a fair share of housing subsidies. However, the $97,000 amount you mentioned is surprising.

HDB uses fixed resale levy amounts. These are based on the type of your first subsidised flat, and if that's an EA, the levy is $50,000.

If you have sold your first subsidised flat from March 3, 2006 onwards, you will pay a fixed amount resale levy as follows:

| First Subsidised Housing Type | Resale Levy Amount | |

| Households | Recipient of CPF Housing Grant (Singles) | |

| 2-room/ 2-room Flexi flat | $15,000 | $7,500 |

| 3-room flat | $30,000 | $15,000 |

| 4-room flat | $40,000 | $20,000 |

| 5-room flat | $45,000 | $22,500 |

| 3Gen flat | $45,000 | Not applicable |

| Executive flat | $50,000 | $25,000 |

| Executive Condominium | $55,000 | Not applicable |

It's possible that, when you were told about the $97,000, it may have been inclusive of other obligations or costs besides the levy itself, such as the refund of any used CPF monies, conveyancing fees, etc.

Under HDB rules, the resale levy must be paid in cash or from the sale proceeds of your existing flat. It cannot be paid using CPF savings or financed with a housing loan.

The timing depends on when you sell your EA:

One final point: the resale levy only applies when you buy another subsidised flat. If instead of a BTO you buy a resale flat without housing grants – or a private property – there would be no resale levy.

The "correct" answer to this varies between individuals. But from personal experience, I find that layout can matter more than size.

Even a "large" resale flat in the central area can feel tighter than some newer flats, despite what the square footage suggests. For example: older flats may technically be bigger, but they're also more likely to have long internal corridors that don't receive natural light. Or they may have segmented spaces that reduce the versatility of the layout (e.g., executive maisonettes often put all the bedrooms on the top floor, which is problematic for older folks who need to climb up to the bedroom.)

This tends to matter more over time, especially if you have work-from-home arrangements, children, or visiting parents who stay over.

That said, older flats do tend to be larger. This is somewhat balanced out by being older, and of course having a higher quantum. But you should also consider that older flats tend to need more extensive renovation: this could add a cost of time as well.

If your primary goal of moving is just reducing commute time, and improving day-to-day convenience, then a newer flat near Tanjong Pagar can be a rational choice. It's probably quicker and cheaper to renovate, and you won't need to worry about lease decay.

But if the main goal is to have a more comfortable, long-term family home – one where you might stay for all of your life, with no concern over resale value (because you're unlikely to ever sell), then a larger unit may be more important.

A big part of this answer unfortunately falls outside of my purview: that's the realm of retirement planning. However, I can give you an example of why different retirement strategies will treat this differently.

Some retirees prioritise cash flow above all else. For this group, selling the condo and downsizing into a flat might be sensible. The freed-up capital can be converted into a predictable income stream, which fits their overall strategy. They also don't need to deal with things like rogue tenants, property market cycles, vacancies, etc.

Others care more about preservation. They'd be comfortable holding on to the freehold condo as a long-term store of value; and the rental income as a way to partially monetise the property while keeping it. Quite likely, they already have income from elsewhere and don't need the rent, but it's a nice-to-have.

It is your chosen retirement strategy that determines the right choice – over and above concerns like the rental yield, or the potential appreciation. It also has to be in line with how much you can actively manage the property in retirement.

As a personal opinion, I would opt to remain a landlord only if I have reliable hands helping me (e.g., trustworthy family members.) I don't really see myself inspecting properties, vetting tenants, or chasing down late rental payments when I'm in my 70s or older. If I don't have the help I need, I'd rather liquidate the rental asset and reinvest in something else.

| Project Name | Price (S$) | Area (Sqft) | $Psf | Tenure |

| Union Square Residences | $18,500,000 | 4833 | $3,828 | 99 yrs (2024) |

| Amber House | $5,398,557 | 1744 | $3,096 | FH |

| Watten House | $4,904,000 | 1539 | $3,186 | FH |

| Grand Dunman | $4,492,000 | 1787 | $2,514 | 99 yrs (2022) |

| Elta | $4,432,000 | 1776 | $2,495 | 99 yrs (2024) |

| Project Name | Price (S$) | Area (Sqft) | $Psf | Tenure |

| Newport Residences | $1,345,000 | 452 | $2,975 | FH |

| Narra Residences | $1,524,000 | 721 | $2,113 | 99 yrs |

| The Lakegarden Residences | $1,592,000 | 678 | $2,348 | 99 yrs (2023) |

| Orchard Sophia | $1,906,000 | 635 | $3,001 | FH |

| Aurea | $1,939,014 | 710 | $2,729 | 99 yrs (2024) |

| Project Name | Price (S$) | Area (Sqft) | $Psf | Tenure |

| Seascape | $5,553,000 | 2669 | $2,080 | 99 yrs (2007) |

| Richmond Park | $5,100,000 | 1550 | $3,290 | FH |

| Scotts Highpark | $4,150,000 | 1744 | $2,380 | FH |

| Amber Point | $4,122,000 | 1690 | $2,439 | FH |

| Scotts Square | $4,080,000 | 1238 | $3,296 | FH |

| Project Name | Price (S$) | Area (Sqft) | $Psf | Tenure |

| Sims Urban Oasis | $885,000 | 441 | $2,005 | 99 yrs (2014) |

| Skies Miltonia | $940,000 | 710 | $1,323 | 99 yrs (2012) |

| J Gateway | $1,050,000 | 474 | $2,217 | 99 yrs (2012) |

| Park Place Residences at PLQ | $1,090,000 | 484 | $2,250 | 99 yrs (2015) |

| Watercolours | $1,120,000 | 915 | $1,224 | 99 yrs (2012) |

| Project Name | Price (S$) | Area (Sqft) | $PSF | Returns | Holding Period |

| Cote d'Azur | $3,220,000 | 1539 | $2,092 | $2,065,000 | 17 Years |

| Amber Point | $4,122,000 | 1690 | $2,439 | $1,922,000 | 9 Years |

| Richmond Park | $5,100,000 | 1550 | $3,290 | $1,800,000 | 19 Years |

| Hundred Palms Residences | $2,130,000 | 1055 | $2,019 | $1,172,200 | 9 Years |

| Calarasi | $1,828,000 | 1227 | $1,490 | $1,143,000 | 19 Years |

| Project Name | Price (S$) | Area (Sqft) | $PSsf | Returns | Holding Period |

| Sescape | $4,050,000 | 2174 | $1,863 | -$1,872,000 | 15 Years |

| Scotts Square | $4,080,000 | 1238 | $3,296 | -$1,175,310 | 19 Years |

| Martin Modern | $2,088,000 | 764 | $2,732 | $97,700 | 7 Years |

| Park Place Residences at PLQ | $1,090,000 | 484 | $2,250 | $155,001 | 9 Years |

| J Gateway | $1,050,000 | 474 | $2,217 | $162,000 | 6 Years |

| Project Name | Price (S$) | Area (Sqft) | $Psf | ROI (per cent) | Holding Period |

| Cote d'Azur | $3,220,000 | 1539 | $2,092 | 179 per cent | 17 Years |

| Calarasi | $1,828,000 | 1227 | $1,490 | 167 per cent | 19 Years |

| Casablanca | $1,280,000 | 1109 | $1,155 | 155 per cent | 24 Years |

| Hundred Palms Residences | $2,130,000 | 1055 | $2,019 | 122 per cent | 9 Years |

| Arc at Tampines | $1,650,000 | 1173 | $1,406 | 95 per cent | 14 Years |

| Project Name | Price (S$) | Area (Sqft) | $Psf | ROI (per cent) | Holding Period |

| Seascape | $4,050,000 | 2174 | $1,863 | -32 per cent | 15 Years |

| Scotts Squsre | $4,080,000 | 1238 | $3,296 | -22 per cent | 19 Years |

| Martin Modern | $2,088,000 | 764 | $2,732 | 5 per cent | 7 Years |

| Affinity at Serangoon | $2,668,000 | 1453 | $1,836 | 9 per cent | 4 Years |

| Perfect Ten | $4,200,000 | 1281 | $3,279 | 10 per cent | 3 Years |

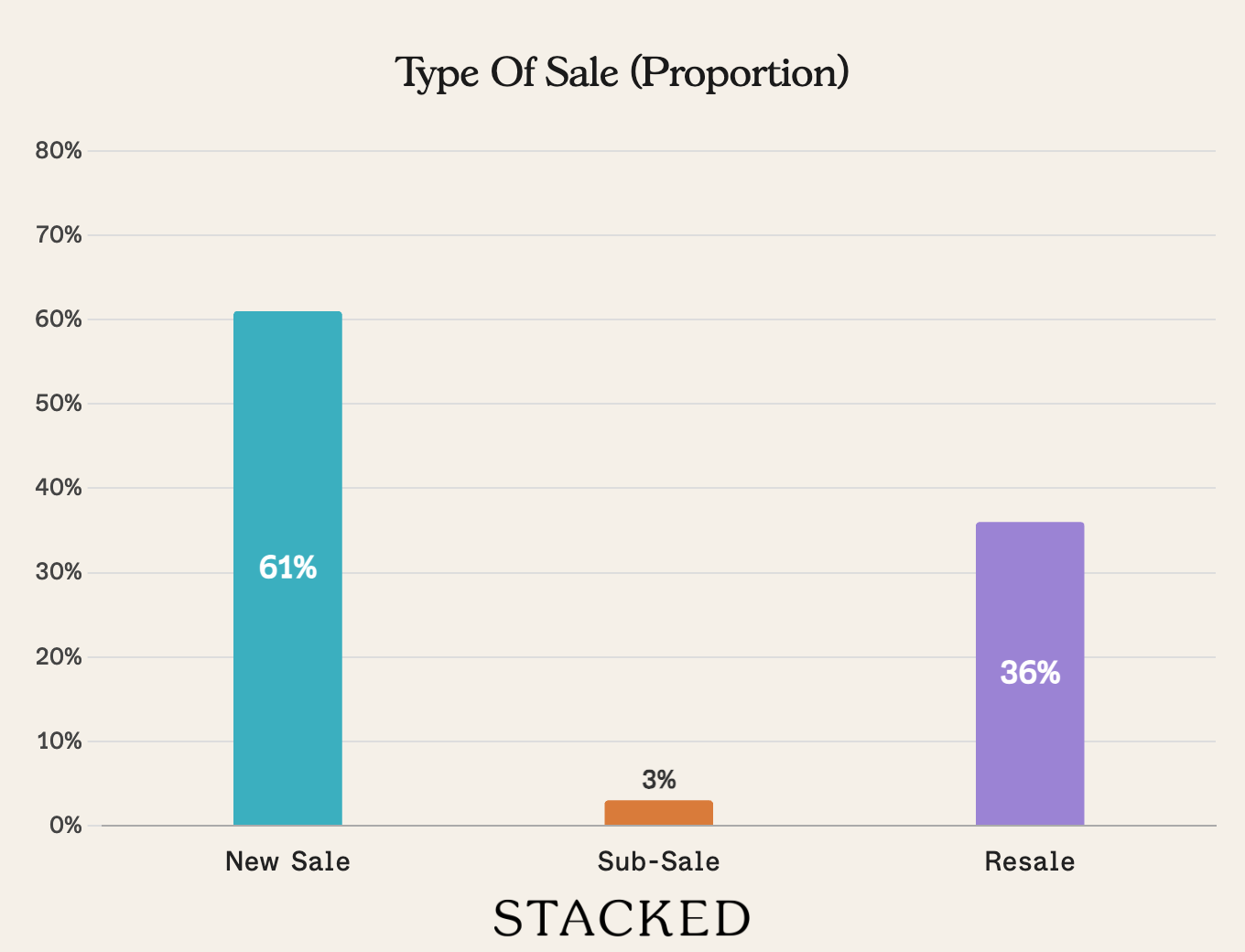

Transaction Breakdown

This article was first published in Stackedhomes.